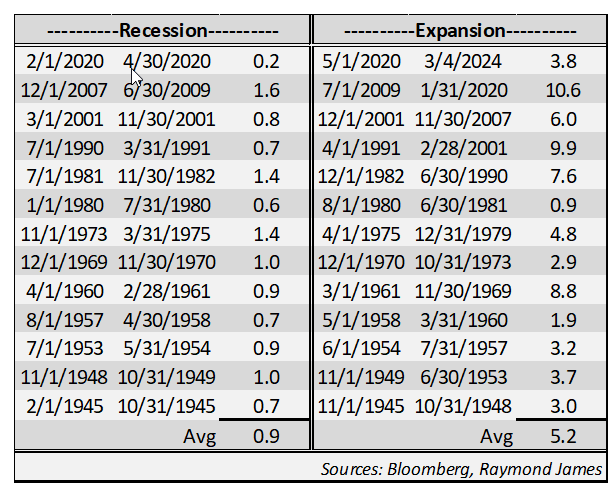

Cycles are long term

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Recessions are part of the economic cycle. No one looks forward to a recession because of the pain it can impose on investors or worse, job security. However, we can tend to overstress about its effect and minimize the potential impact of the long-term benefits of economic turnover. Recessions occur because something is out of whack. Interest rates are too high, a black swan event occurs (i.e. a pandemic), or inflation remains too high for too long causing consumers to stop spending. A recession can “reset” the market.

Higher interest rates often precede a recession. This is good for savers. If a recession occurs, the Fed typically eases its policy by lowering interest rates. This can help the mortgage market and create opportunities for other asset classes. It allows cheaper borrowing and expansion potential.

On average, recessions last less than a year. In comparison, expansions have lasted more than 5 years. One could argue that the Fed, by using more of its policy tools, has found ways to prolong expansionary periods without measurable recessionary consequences. The last 5 recessionary periods have averaged 0.9 years, the same average going back to 1945. On the other hand, the last 5 expansionary periods have averaged 7.6 years (and this one is still in progress), 46% longer than the average from 1945.

A recent black swan event, COVID-19, caused a mini-recession. It also changed consumer behavior. Businesses shut down and consumers brought savings to unprecedented levels. The government pumped money into the system, even directly into consumer pockets. As things turned, consumers spent a lot of money collapsing their record savings to below long-term averages. The current consumer spending behavior has depleted savings, used up government handouts, and continued to spend on borrowed money. Revolving credit is reaching record levels. Despite the euphoric media mantra proclaiming a robust economy and recession defeat, the strength of this growth might be built on a house of cards.

All of this said, my intent is not to build a case for or against an upcoming recession. What matters most is what we all know – for fixed income investors, yields are high and that spells opportunity for investors. Cycles are long as shown above. As an investor, are you “trading” or “investing”? Traders live in the moment and attempt to time the market and take advantage of day-to-day price actions. Most of our readership invests. They look to long-term strategies that protect capital. Today’s investments allow asset protection and an opportunity to lock into higher levels of known income and cash flow for long-term benefit.

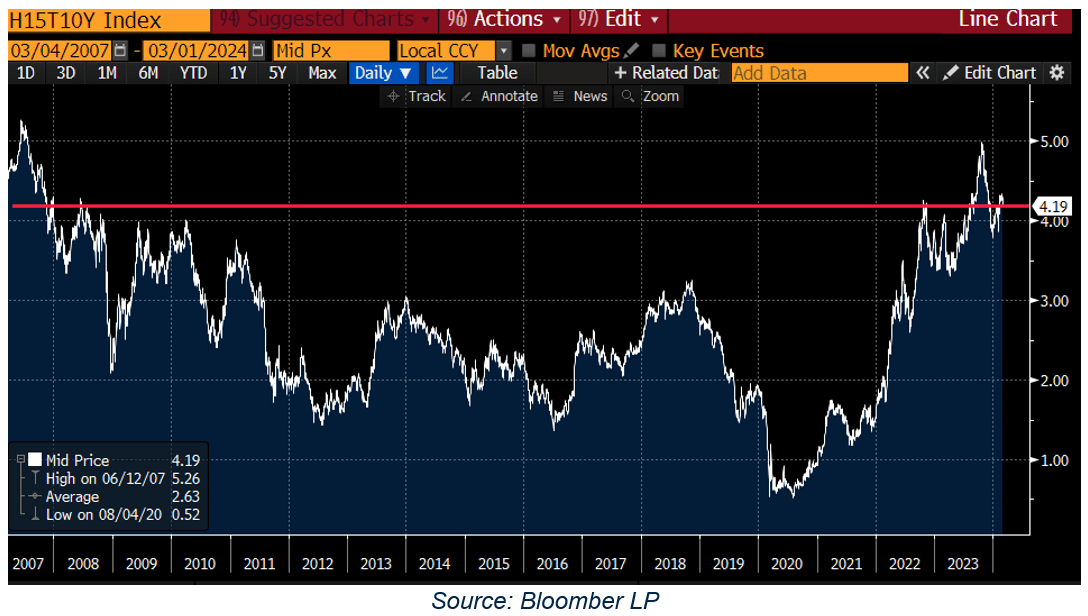

Economic cycles are long. Fixed income investing also entails a long-term strategy. Rates remain at levels not consistently seen in nearly 2 decades (17+ years). The graph shows the yield movement of 10-year Treasury rates. Avoid the short-term timing temptations and look to lock in for longer while the opportunity exists.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.